- A booming post-COVID economy could lead to a short economic cycle that leads to higher inflation and interest rates, according to Morgan Stanley.

- The bank recommends investors trim equities and fixed income exposures as they face early-cycle timing, increasingly mid-cycle conditions and late-cycle valuations.

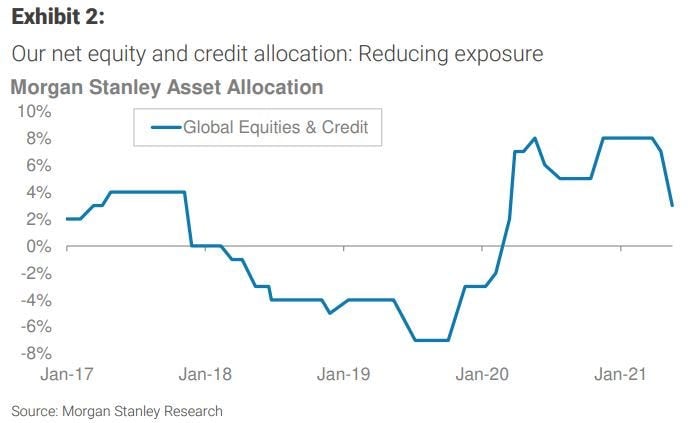

- "We are reducing exposure to credit and equities and reducing our underweight to cash, a move we think is supported by cycle-adjusted risk premiums," Morgan Stanley said.

- Sign up here for our daily newsletter, 10 Things Before the Opening Bell.

More than one year removed from the height of the COVID-19 pandemic, the economic recovery is in full swing, according to a Sunday note from Morgan Stanley.

But in a world where the economy is running hot, investors have a lot to juggle in terms of rising inflation, tighter monetary policy from central banks, and the potential for margin pressure and higher corporate tax rates.

"Just 14 months from the lows, investors face early-cycle timing, increasingly mid-cycle conditions and late-cycle valuations," Morgan Stanley analyst Andrew Sheets said.

Given the complicated backdrop, the bank recommends investors reduce exposure to both credit and equities, according to the note.

"The bulk of our reduction is in credit, which our credit strategists are downgrading. The asset class has had an outstanding run, but is both expensive and disadvantaged in a hotter cycle," Morgan Stanley explained.

The bank also lowered US equities to neutral, and now favors international stocks over US stocks, the note said.

Global equities ex-US have more elevated risk premiums, better mid-cycle performance and higher 12-month forecasted returns relative to other asset classes, according to the bank.

"Our top region is Europe, followed by Japan, as both regions have less inflationary pressure, less risk of changing tax or central bank policy, and less expensive valuations," the bank argued.

But if central banks continue to enact easy monetary policies even in the face of booming growth and higher inflation, than stocks could continue to run higher, as they did in the late 1990's.